33%

Of US VC $ to top 1% of companies, 2025

12%→33%

Same figure in 2022

67%

Of VC $ outside that top 1%

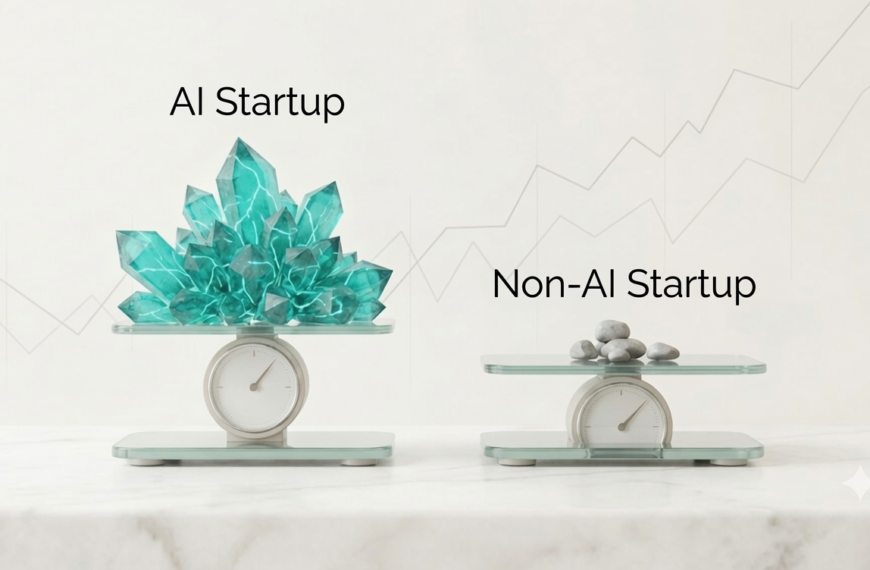

222%

AI valuation premium at Series D+, 2025

- What “Startup Theater” Actually Meant

- The Barbell Market: Concentration at the Top, Discipline Everywhere Else

- What Actually Changed in How Investors Evaluate

- Milestone-Based Funding Replaces the War Chest Mentality

- The AI Exception — And Why It Isn’t Really an Exception

- The 67% Nobody’s Writing About

- Verdict

- MORE ON BUSINESS & STARTUPS

What “Startup Theater” Actually Meant

For most of the last decade, a certain kind of founder could raise serious money on the strength of a story alone. A confident founder, a big total-addressable-market slide, a growth trajectory drawn with a ruler and a lot of optimism — and millions would follow, often before there was a working product, let alone paying customers.

That era had a name behind closed doors: growth-at-any-cost. The metric that mattered wasn’t profitability or even unit economics — it was velocity. How fast could you spend to grow, and how big could the next round be. The performance of fundraising itself — the deck, the narrative, the “vision” — became indistinguishable from the business it was supposed to represent. Hence “startup theater”: founders performing momentum for an audience of investors who, for a few years, were happy to buy tickets.

“Not long ago, a charismatic founder with a big idea could raise millions on vision alone. But after the boom-and-bust cycle of the early 2020s, today’s investors have a new playbook.” — SeedScope, What Investors Want in 2026

The correction that followed — the 2022–2023 rate hikes, the LP pullback, the wave of down rounds and quiet shutdowns — didn’t just cool the market. It rewrote the rules for what “fundable” means, and those rules are now fully in force.

The Barbell Market: Concentration at the Top, Discipline Everywhere Else

The defining structural fact of 2026 venture capital is concentration. According to Silicon Valley Bank’s H1 2026 State of the Markets report, 33% of all US VC dollars went to the top 1% of companies by valuation in 2025 — up from just 12% in 2022. Mega-rounds for a handful of frontier AI companies are absorbing a wildly disproportionate share of total capital.

SVB describes this as a “barbell” market: massive late-stage rounds concentrated in a tiny number of mostly-AI companies on one end, and tightly disciplined, “pre-consensus” early-stage investing on the other — with a hollowed-out middle in between. The mega-round headlines are real, but they describe an increasingly narrow slice of the actual venture landscape.

WHAT “PRE-CONSENSUS” INVESTING MEANS IN PRACTICE

Early-stage investors increasingly look for bets the broader market hasn’t yet recognized or priced in — meaning conviction has to come from genuine diligence on the business, not from chasing a category that’s already attracting consensus capital. This is the opposite of theater: it requires investors to do real homework on companies nobody else is excited about yet, and it requires founders to have real evidence to show, since there’s no hype wave to ride.

What Actually Changed in How Investors Evaluate

The mechanics of diligence have shifted from “does this story make sense” to “can this team execute and survive.” A few concrete changes show up across nearly every report on 2026 fundraising:

The Discipline Era (2025–2026)

- Real revenue, signed pilots, and retention data drive valuation

- Raise only what’s needed to hit the next milestone

- CAC, burn multiple, and path to profitability are scrutinized

- Investors expect a specific 4-quarter KPI plan tied to the raise

- Late-stage rounds expect public-company-level documentation

The Theater Era (2019–2021)

- Vision and TAM slide drove valuation

- Raise as much as possible, as early as possible

- Growth velocity mattered more than margins

- Vague “use of funds” was acceptable

- A confident narrative could substitute for traction

One line from a 2026 industry analysis captures the shift precisely: investors in 2025 were looking for “clear metrics, lean teams, and smart spend” as signs of operational discipline. Founders who can show they cut a poorly-converting marketing channel, or doubled down where customer acquisition cost was lowest, are demonstrating exactly the kind of capital stewardship that gets rewarded now — where in 2021, that same conversation might never have come up at all.

Milestone-Based Funding Replaces the War Chest Mentality

Perhaps the most concrete structural change is how the money itself gets released. VCs are increasingly writing term sheets that tie funding to milestones rather than handing over a full war chest upfront — releasing capital in tranches as founders hit specific, pre-agreed targets.

This staged approach changes the entire psychology of a raise. Valuations step up as execution is proven, rather than being priced entirely on a future the company hasn’t built yet. It spares founders some of the pressure of unrealistic expectations baked into a single, oversized check — and gives investors confidence that the price they’re paying at each stage actually reflects progress made, not just a story told.

“The era of growth-at-any-cost is over; 2026’s venture dollars are chasing startups that solve tangible problems and can eventually stand on their own financially.” — Veteran VC, quoted in SeedScope’s 2026 Funding Trends report

The practical founder advice circulating in 2026 reflects the same discipline: build proof before you build pitch theater, prepare a clean data room early, get brutally honest feedback before fundraising even starts, and stop asking whether investors are “excited” — start asking whether they’re convinced. That’s a meaningfully different bar than the one that governed 2021.

The AI Exception — And Why It Isn’t Really an Exception

It would be easy to look at AI’s enormous valuation premiums and conclude that discipline doesn’t apply to the hottest category in venture. The opposite is closer to the truth.

AI valuation premiums versus non-AI business models reached 222% at Series D+ in 2025, with triple-digit premiums showing up even at earlier stages. But the founders actually capturing that premium are being scrutinized on fundamentals just as hard, if not harder, than everyone else. Investors have become explicit that simply adding “AI” to a pitch deck doesn’t unlock the multiple — they’re asking specifically whether a company has proprietary data, real distribution, workflow lock-in, cost advantages, or regulatory defensibility. Without that, as one 2026 venture analysis put it bluntly, you’re “just another wrapper business in a crowded queue.”

So the AI premium isn’t evidence that theater still works — it’s evidence that the bar moved everywhere, including the one category still attracting genuine excitement. AI companies command premium multiples due to growth potential, yet investors scrutinize burn rates, CAC, and paths to profitability more rigorously than during the 2021 boom — meaning today’s AI founder has to defend the financial discipline of the business, not just the size of the vision.

The 67% Nobody’s Writing About

The mega-round headlines dominate coverage for an obvious reason — they’re the biggest, most dramatic numbers in any given quarter. But they describe a thin slice of the actual market. 67% of US VC dollars flow outside the top 1% of companies the headlines obsess over — and that’s where the discipline-driven shift is most visible and most consequential for the average founder.

| Era | Top 1% share of US VC $ | Dominant founder behavior |

|---|---|---|

| 2022 | 12% | Broad-based funding, story-driven pitches still common |

| 2025 | 33% | Capital concentration; everyone else competes on fundamentals |

For founders operating in that 67%, the message is double-edged but ultimately favorable to anyone willing to do the work. SVB’s own framing captures it well: “For those focused on the fundamentals rather than the headlines, there’s never been a better time to find overlooked gems, build with discipline and generate outlier returns.” The bar is higher than it was in 2021. It is also, by most accounts from the founders and investors actually operating in this market, clearer — fewer vague promises, more specific expectations on both sides of the table.

Verdict

THE LUDICARC TAKE

The mega-round headlines and the discipline narrative aren’t actually in tension — they’re two views of the same bifurcated market. A small number of frontier AI companies are absorbing record capital at record valuations, and that’s the story most coverage tells. But underneath that, in the 67% of the market that doesn’t make headlines, the operating standard has genuinely changed: milestone-based funding, scrutinized burn rates, real retention data, and a documented path to profitability are now table stakes at every stage, not just at IPO.

For founders, the practical implication is straightforward even if the discipline required is not easy: a confident narrative is no longer sufficient currency. Investors in 2026 are buying risk-adjusted belief, not vision alone — and the companies that will look back on this period as a golden era of company-building are the ones treating that distinction as the actual rules of the game, not an obstacle to talk their way around.